Distributing Cash to Shareholders: Dividends and Share Buybacks

Weekly updates on the innovation economy and market commentary.

Introduction

Today’s blog post discusses the concept of distributing cash to shareholders, with specific emphasis on the following five topics:

Distributing Cash to Shareholders via Dividends and Share Buybacks

Monetary Policy and Its Impact on Market Liquidity

Liquidity to Shareholders

Performance of Sample Dividend-Focused Index Funds

Apple Case Study: Accelerating EPS Growth with Share Buybacks

Monetary Policy Impacts Market Liquidity

Notably in 2022, the unwinding of expansionary monetary policy occurred, and the Federal Reserve’s monetary policy stance pivoted towards a restrictive monetary policy environment with rising interest rates.

Volatility and liquidity often are inversely connected. Restrictive monetary policy causes increased volatility in financial markets because the central bank is draining excess liquidity from financial markets when it increases interest rates, reduces the size of the Fed balance sheet, reduces the growth rate in M2 money supply, tightens financial conditions, and implements Quantitative Tightening (QT).

Investors in companies that need liquidity often invest in these unprofitable companies when the exit liquidity (future selling price) is very high or when an external source (such as expansionary monetary policy from the Federal Reserve or government grants) are providing the funding source (either influenced indirectly or directly) for the added liquidity. When these sources of liquidity largely dry up in this current 2022 environment, the resulting consequence is falling stock prices and low IPO activity.

Liquidity to Shareholders

Companies with large balance sheets and positive operating income can create liquidity for their own stock via share buybacks.

Stronger companies with large balance sheets can create liquidity for other stocks by buying minority interests or making acquisitions.

Companies that provide liquidity to their shareholders via distributing cash through cash dividends and share buyback programs are valuable to investors. In contrast, companies that require liquidity from financial markets (such as unprofitable companies that need frequent external financing from equity investors through equity dilution & fundraising) are draining investor liquidity and therefore is not well appreciated by investors when there is a scarcity of liquidity, thereby contributing to plummeting stock prices for many unprofitable companies when there is restrictive monetary policy, tight credit creation, and when the availability, affordability, and accessibility of capital are low.

Rising dividends over time are valuable to investors because investors receive more liquidity (cash) directly from the company over time, which can then be reinvested back into the company’s stock, reinvested in other assets, spent in the real economy, or used for other purposes.

Company fundamentals indirectly provide liquidity for the company’s stock (via investor demand that likes the narrative of strong fundamentals) and/or directly provide liquidity directly to shareholders (via dividends and share buybacks that are financed by operating profits from the company or debt financing). From an equity shareholder perspective, a corporation is a machine that absorbs and distributes cash; the value of a company increases when it has a perceived or actual ability to distribute high and growing cash flows at low discount rates.

Dividends Provided Benchmark-Beating Performance So Far in 2022

Sample Index Fund Ticker Symbols:

VOO is an index fund ticker symbol for Vanguard’s S&P 500 index fund. SPX is the index ticker symbol for the S&P 500 Index.

VYM is an index fund ticker symbol for Vanguard’s dividend-focused stock index fund.

SCHD is an index fund ticker symbol for Charles Schwab’s dividend-focused stock index fund.

Key Insights:

As displayed by the above Koyfin chart, VYM and SCHD are examples of dividend-focused index funds that performed better than the S&P 500 Index in the first 11.5 months of 2022.

We are of the opinion that this performance divergence between dividend-focused funds and popular stock market indices so far in 2022 is not a coincidence.

Dividends provide liquidity (cash) to shareholders. The desire and demand for liquidity from investors, which may be displayed in the form of higher prices for assets that provide liquidity to investors, often increases in environments with volatile bear markets, high investment uncertainties, restrictive monetary policy that drains liquidity from markets, and higher discount rates when making new investments.

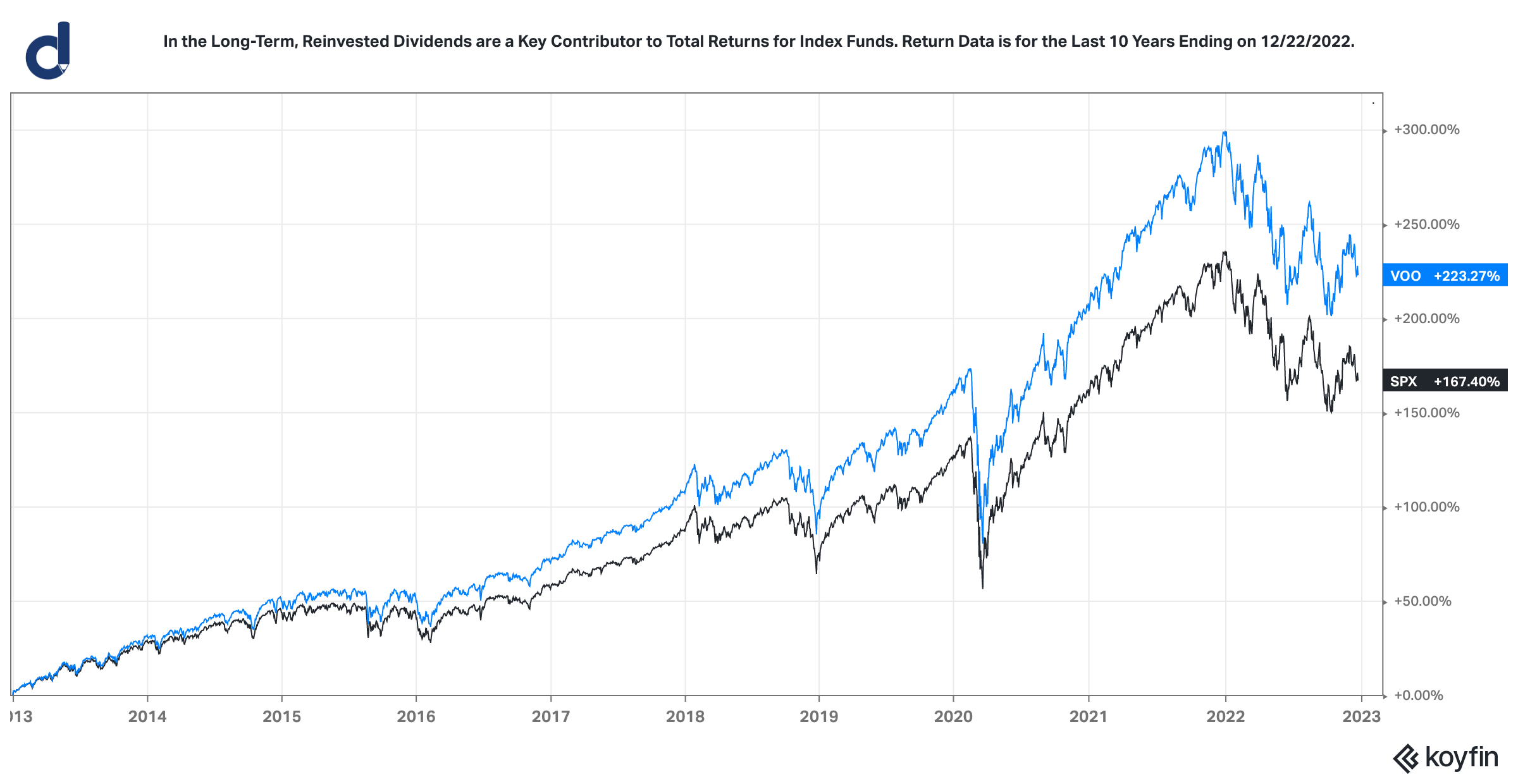

The Power of Dividends

The above Koyfin chart graphs the year-to-date performance (as of December 22, 2022) for the S&P 500 Index (SPX) and for Vanguard’s S&P 500 Index Fund (VOO).

Key Insights:

In the short-term, the performance of a quality index fund with dividends often closely tracks the performance of a benchmark price index.

In the long-term, the power of dividends is valuable to investors. In the long-term, dividends are often a key contributor to total returns, and an index fund with reinvested dividends over time can perform better than a related benchmark price index, as seen in the chart below:

Apple Case Study: Accelerating EPS Growth with Share Buybacks

When a company has growing margins and earnings, then the company can accelerate the growth rate in earnings per share (EPS) via share buybacks. Apple is a great example of this situation; from fiscal year 2020 to fiscal year 2022:

Apple’s gross margin increased from 38.2% to 43.3%.

Apple’s revenue increased by about 44%.

Apple’s operating income increased by about 80%.

Apple’s earnings per share increased by about 86%.

Share count reduced by about 7%, enabling rising corporate earnings to accrue to less shares, thereby accelerating the growth in earnings per share.

In fiscal year 2022, Apple spent about $90 billion in share repurchases and distributed about $15 billion in cash dividends to shareholders.

Data Sources: Apple’s Fiscal Year 2022 10K Filing, https://investor.apple.com/investor-relations/default.aspx and https://s2.q4cdn.com/470004039/files/doc_financials/2022/q4/_10-K-2022-(As-Filed).pdf

Concluding Thoughts

In a restrictive monetary policy environment with market volatility, elevated inflation, and geopolitical uncertainty, discount rates for investors increased, and liquidity was increasingly desirable by investors. As a result, the divergence in stock performance was significant in the past year: several stocks of companies that provided significant liquidity to shareholders via dividends and share buybacks performed better in the past year compared to the price performance of several stocks of high-priced unprofitable companies.

Dividends and share buyback programs are methods of companies distributing cash to shareholders.

Dividends provide ongoing dividend income to shareholders, which is particularly useful for income-focused investors. Dividends can be reinvested, re-allocated to other investments, spent in the real economy, or used for other purposes.

Stock buybacks may be utilized as a valid financial capital allocation strategy, be used to fully or partially offset the dilution from stock-based compensation expenses, and may accelerate the EPS growth in an already-growing earnings per share for the company.

In the long term, an important component of total returns to shareholders are derived from capturing the benefits of share buybacks and dividends.

References:

Apple’s Fiscal Year 2022 10-K Financial Filing, Announced on 10/27/2022, https://s2.q4cdn.com/470004039/files/doc_financials/2022/q4/_10-K-2022-(As-Filed).pdf

Apple Investor Relations, https://investor.apple.com/investor-relations/default.aspx

Koyfin, https://www.koyfin.com/home

This letter is not an offer to sell securities of any investment fund or a solicitation of offers to buy any such securities. An investment in any strategy, including the strategy described herein, involves a high degree of risk. Past performance of these strategies is not necessarily indicative of future results. There is the possibility of loss and all investment involves risk including the loss of principal.

Any projections, forecasts and estimates contained in this document are necessarily speculative in nature and are based upon certain assumptions. In addition, matters they describe are subject to known (and unknown) risks, uncertainties and other unpredictable factors, many of which are beyond Drawing Capital’s control. No representations or warranties are made as to the accuracy of such forward-looking statements. It can be expected that some or all of such forward-looking assumptions will not materialize or will vary significantly from actual results. Drawing Capital has no obligation to update, modify or amend this letter or to otherwise notify a reader thereof in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate.

This letter may not be reproduced in whole or in part without the express consent of Drawing Capital Group, LLC (“Drawing Capital”). The information in this letter was prepared by Drawing Capital and is believed by the Drawing Capital to be reliable and has been obtained from sources believed to be reliable. Drawing Capital makes no representation as to the accuracy or completeness of such information. Opinions, estimates and projections in this letter constitute the current judgment of Drawing Capital and are subject to change without notice.