Introduction

With supporting data visualizations from a series of charts, today’s newsletter compares the Dow Jones Industrial Average (“DJIA”) versus the NASDAQ 100 Index (“NDX”).

Historically over a longer investment time horizon, NDX has mostly enjoyed higher performance than DJIA. If one is of the opinion that technology-enabled growth companies will continue to create high shareholder value in the future, then it is possible that the historical positive performance differentiation of the NDX over DJIA may persist in the future.

Dow Jones Industrial Average (“DJIA”) and NASDAQ 100 Index (“NDX”):

DJIA is a price-weighted stock market index with 30 components. Additional information and data about this index can be found on the S&P Global website, https://www.spglobal.com/spdji/en/indices/equity/dow-jones-industrial-average/#data

NDX is a stock market index with a large weight to technology companies. According to the creator of the NASDAQ 100 Index, NDX “is designed to measure the performance of 100 of the largest Nasdaq-listed non-financial companies”. Additional information, data, and the source of this quote can be found on the NASDAQ website, https://indexes.nasdaq.com/docs/Methodology_NDX.pdf

The SPDR Dow Jones Industrial Average ETF under ticker symbol “DIA” is a popular index fund that seeks to track DJIA.

The Invesco NASDAQ 100 ETF under ticker symbol “QQQ” is a popular index fund that seeks to track NDX.

Quick Note on Stock Market Indexes

The number of stock market indexes to track various components of the stock market has dramatically increased in the past decade. Interestingly and according to both a Bloomberg article in 2017 and this supporting chart from Bloomberg, “the number of market indexes now exceeds the number of U.S. stocks”. Source: https://www.bloomberg.com/news/articles/2017-05-12/there-are-now-more-indexes-than-stocks

Popular US Stock Market Indexes:

Dow Jones Industrial Average

S&P 500 Index

NASDAQ 100 Index

Russell 2000 Index

Today’s newsletter will focus on the Dow Jones Industrial Average (“DJIA”) and NASDAQ 100 Index (“NDX”).

Performance Returns

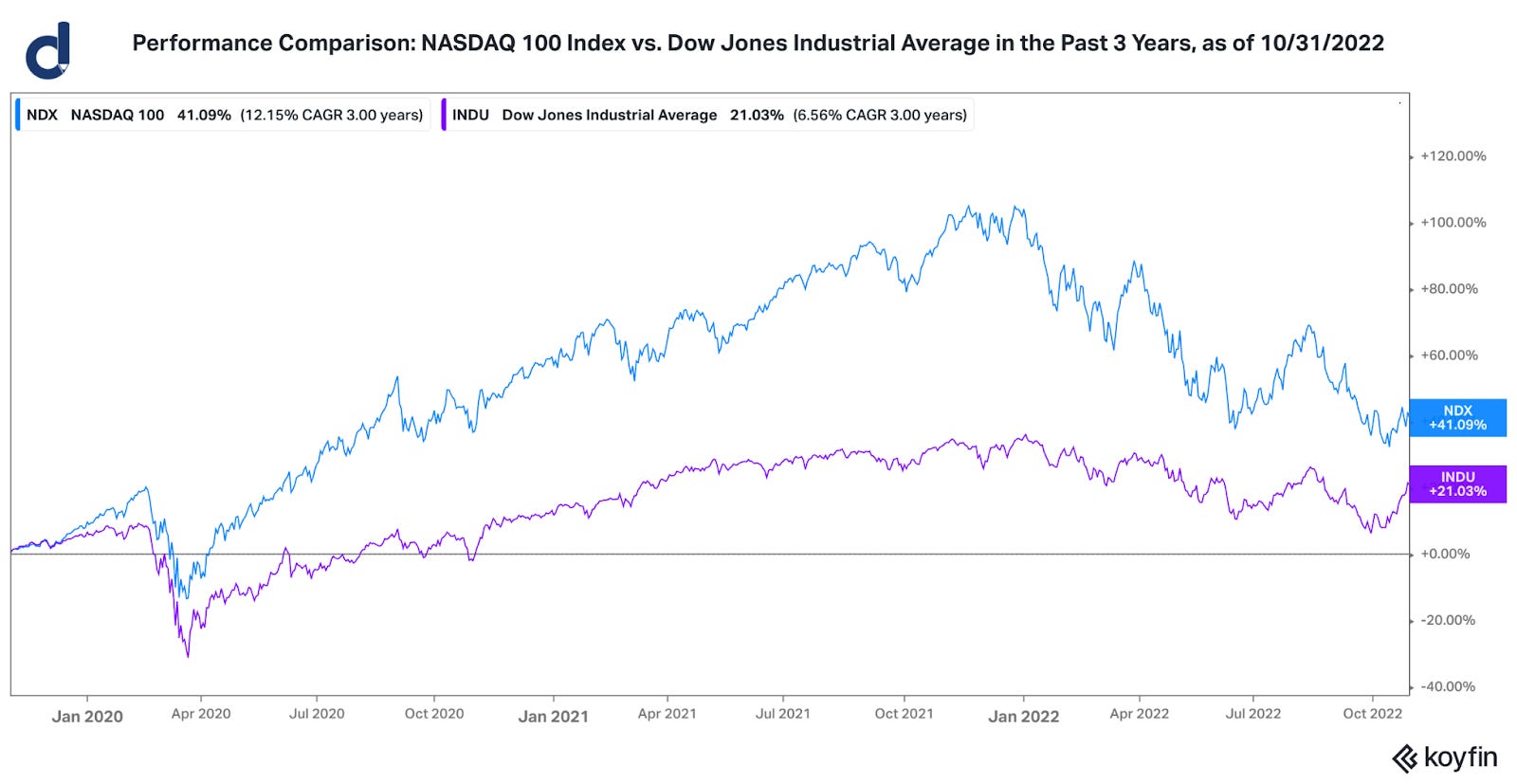

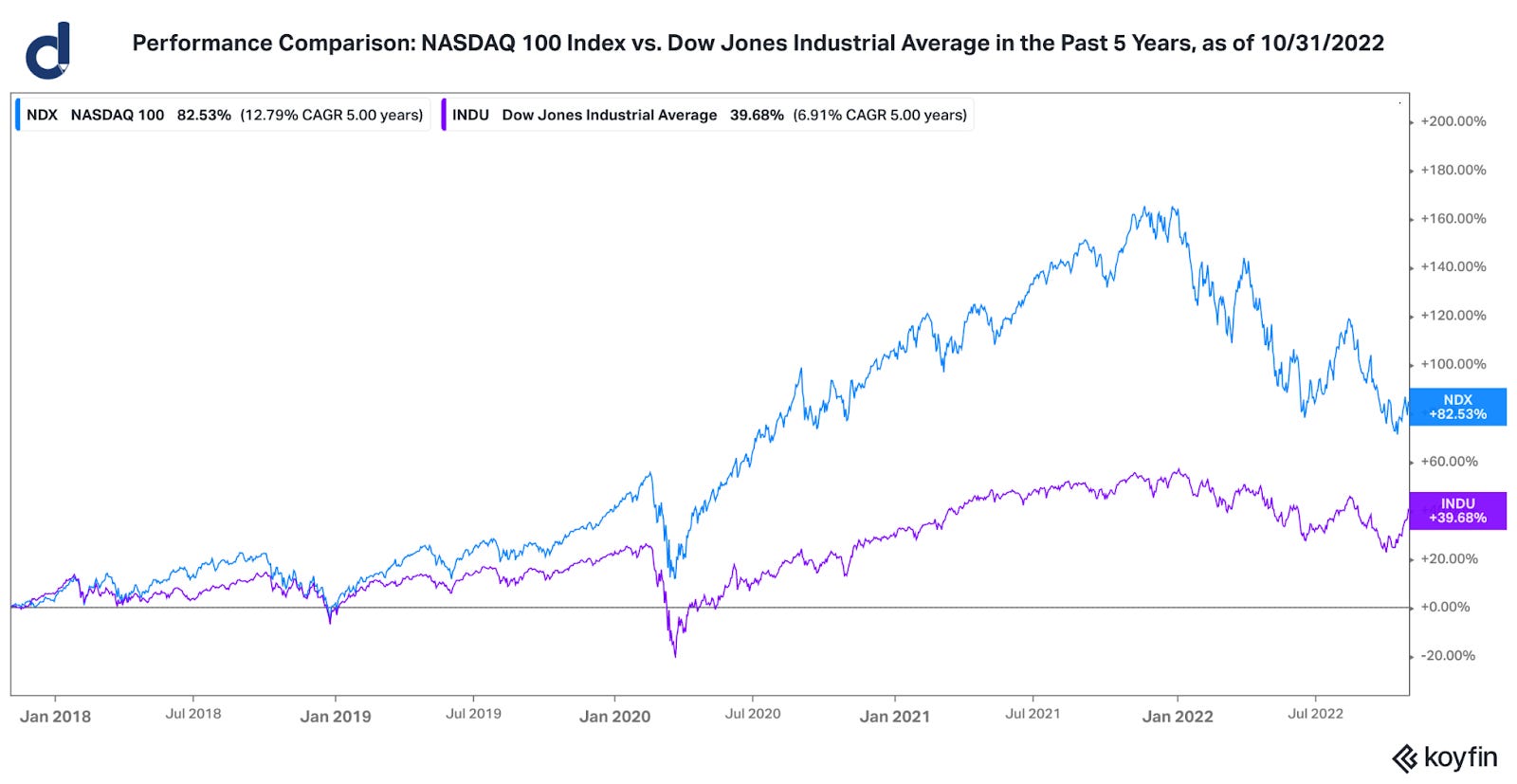

Across trailing 3-year, 5-year, 10-year, and 20-year time horizons, the NASDAQ 100 Index (NDX) has historically performed better than the Dow Jones Industrial Average (DJIA), as seen by the four following charts:

3-Year Performance Comparison:

5-Year Performance Comparison:

10-Year Performance Comparison:

20-Year Performance Comparison:

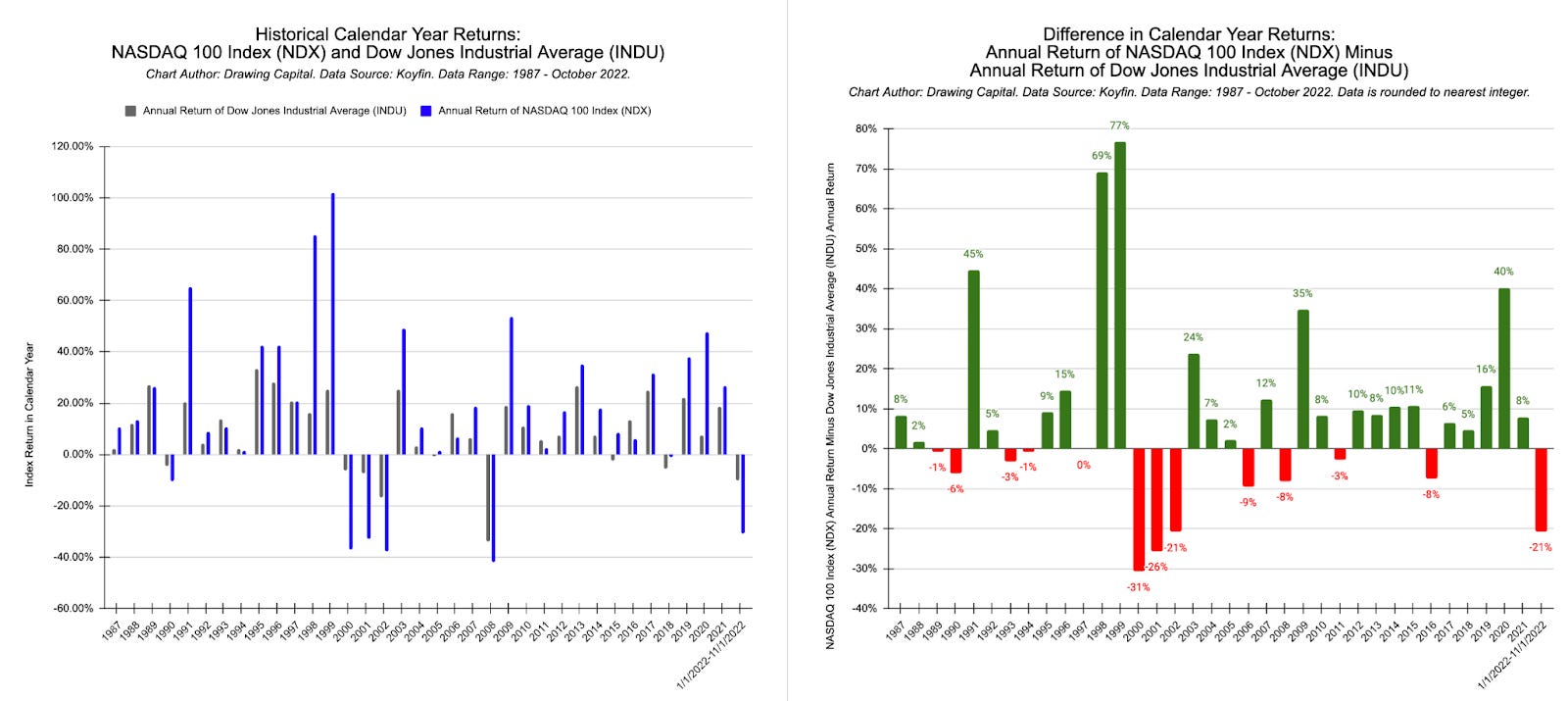

Comparison of Annual Returns: DJIA vs. NDX

Key Insights:

From 2009-2021, NDX significantly benefited from the combination of expansionary monetary policy from the Federal Reserve and strong financial fundamentals (such as growth in revenues, earnings, and dividends paid to shareholders) in many of the underlying companies in NDX.

Significant streaks of positive performance can attract capital inflows into an asset class or industry. According to data from Koyfin, from 2009-2021, NDX had only 1 negative-performing calendar year (occurred in 2018), and this 2018 calendar year was a very small loss (smaller than -2% loss in 2018).

Since 1987, NDX has a history of frequently performing better than DJIA when measuring calendar year performance.

As of 10/31/2022, the performance difference between NDX and DJIA so far in 2022 has been at its worst over the past 15 years from NDX’s perspective (NDX annual return minus DJIA annual return). The last time NDX’s underperformance against the DJIA was this low was during the bursting of the internet tech bubble in 2000-2002, as seen in the red column bars in the chart above.

Comparison of Monthly Returns: DJIA vs. NDX

Key Insight: Reviewing the above scatter plot, a positive relationship exists between the monthly calendar returns for DJIA and NDX. From January 1986 to October 2022, there is a nearly 0.73 correlation between monthly DJIA returns and monthly NDX returns.

Key Insights:

The blue column chart visualizes the difference (performance spread) between NDX’s monthly returns and DJIA’s monthly returns from January 1986 to October 2022. During this measured time period, the average monthly performance difference was about 0.46%, highlighting that NDX performs better than DJIA on average in calendar months.

Since 1986, NDX’s worst monthly performance difference compared to DJIA was -22.8%, which occurred in the month of February 2001.

Since 1986, NDX’s best monthly performance difference compared to DJIA was nearly 27%, which occurred in February 2000.

Key Insights:

The red bar chart displays among the 20 worst monthly performance differences for NDX when compared to DJIA since 1986. In contrast, the green bar chart visualizes the 20 best monthly performance differences for NDX when compared to DJIA since 1986.

The occurrences of the top 20 monthly outperformance of NDX over DJIA all occurred many years ago. None of the months between November 2000 - October 2022 are on the “top 20” list of the highest NDX outperforming months compared to DJIA, as displayed by the months on the green bar chart.

Last month (October 2022) ranked as the 8th worst month in the performance spread difference in (NDX - DJIA) performance since 1986.

Interestingly, there is a time clustering of performance spreads between NDX & DJIA, as seen by the fact that:

The top 7 negative monthly performance differences all occurred between 2000-2002, which was when the internet tech bubble burst.

The lead-up to the peak of the tech bubble (1997- March 2000) enjoyed several strong performance months for NDX.

Importance of Dividends

Dividend income can be a key contributor to total returns. Additionally:

Reinvested dividends can enjoy positive compounded growth in returns when returns are positive.

Dividend income is often less volatile than stock price fluctuations. Dividend-focused investors have positive perceptions about steady and rising dividend income over time from their investments, even if there are minor stock price fluctuations in the short-term.

Usually, a change in stock price doesn’t change the dividend policy of the company (ex. just because a stock falls 10% doesn’t necessarily imply that the next cash dividend payment would be 10% less than last time).

Dividend payments to shareholders are announced by companies and ETF providers and often have a pre-set payment schedule. Investors can choose to reinvest dividend income or keep the cash from cash dividend payments. This choice provides flexibility and income to investors.

Reviewing the Koyfin chart below, notice how QQQ has performed better than NDX, and notice how DIA has performed better than DJIA in the past 20 years. For a quick review, QQQ is an index fund ticker symbol that seeks to track NDX, and DIA is an index fund ticker symbol that seeks to track DJIA. The receipt and reinvestment of dividends from QQQ and DIA have added to price returns for calculating total-return fund performance over the past 20 years.

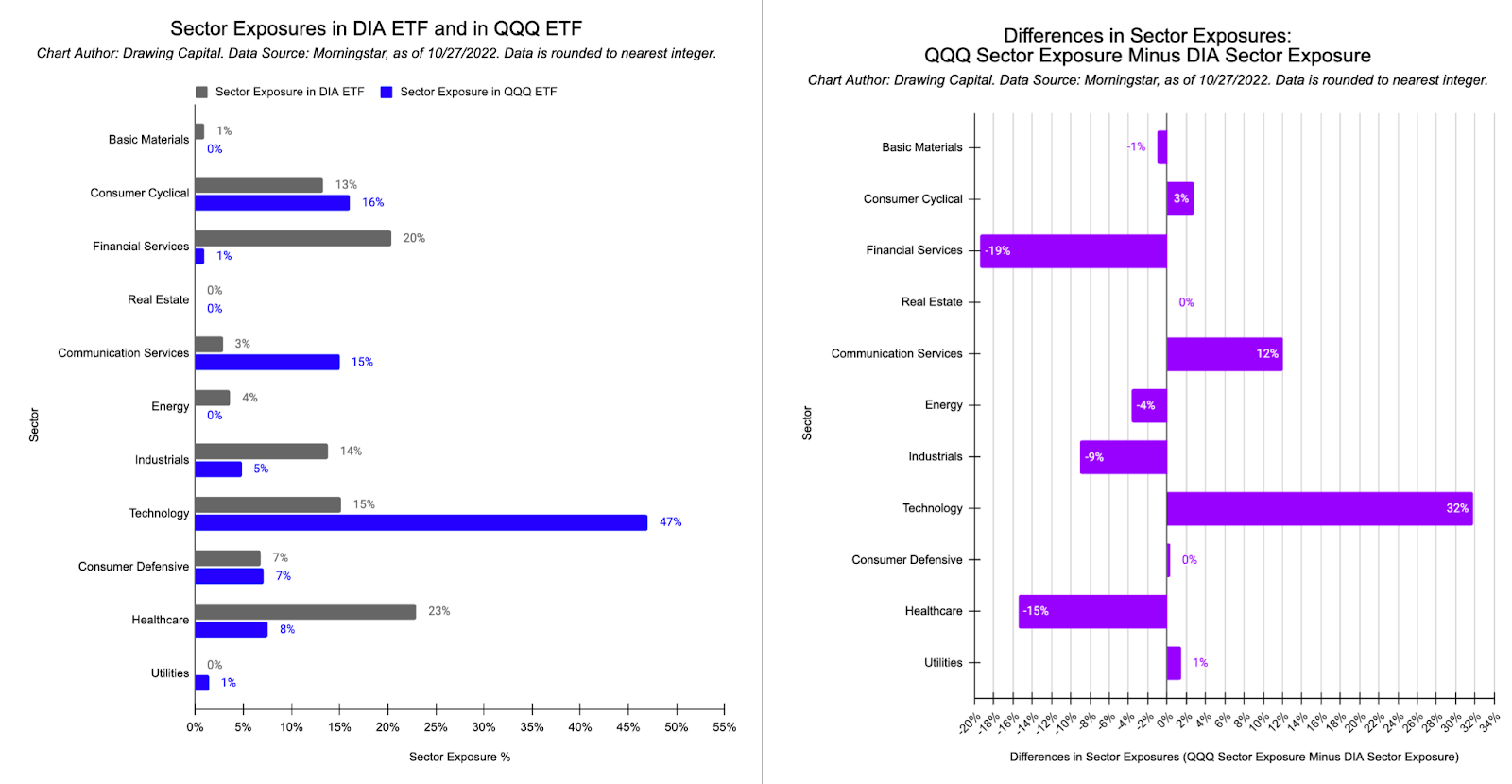

Sector Exposures in DIA ETF and QQQ ETF

Key Insights from the above chart:

Similarities: QQQ and DIA have similar percentage weights in the following sectors: utilities, consumer defensive, real estate, and basic materials.

Largest Sector Percentage Weights: The 3 largest sector exposures in QQQ are technology, consumer cyclical, and communication services. In contrast, the 3 largest sector exposures in DIA are healthcare, financial services, and technology.

QQQ has significantly more sector exposure in technology and communication services compared to DIA.

QQQ has significantly less sector exposure in financial services, industrials, and healthcare compared to DIA.

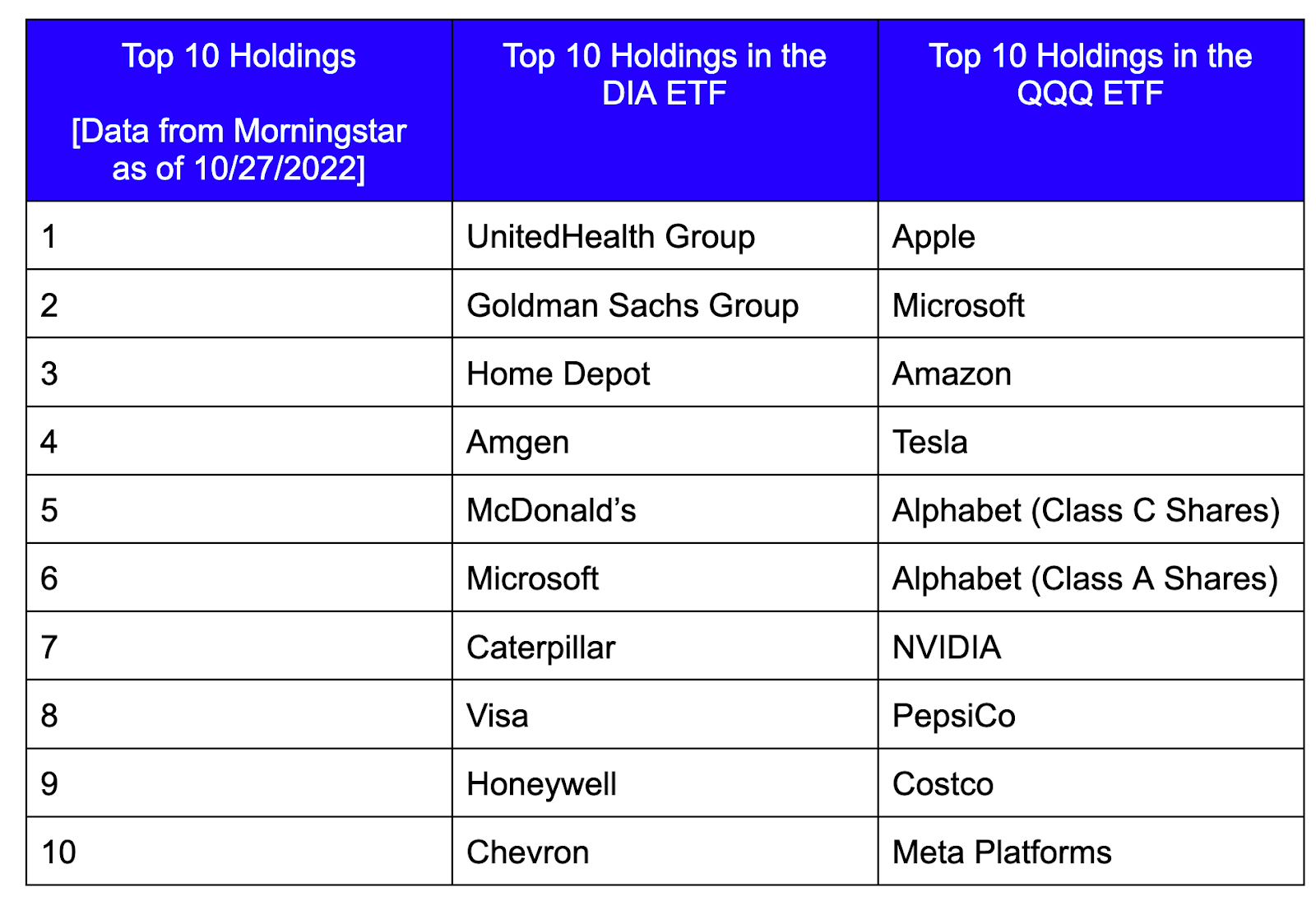

Top 10 Holdings

Key Insights:

Microsoft: According to portfolio composition data from Morningstar, Microsoft is the only overlapping company from the above list (as of October 27, 2022) for the top 10 holdings of the DIA index fund and QQQ index fund. Said differently, even though both DIA and QQQ are considered to be “large cap index funds”, their top 10 positions have little overlap.

Technology Industry Exposure: It is clear that QQQ has significant technology company exposure, as seen by Apple, Microsoft, Amazon, Tesla, Alphabet, NVIDIA, and Meta Platforms all being featured in the top 10 holdings of QQQ.

Fund Concentration: According to data from Koyfin, the top 10 holdings have a nearly 50% weight in the QQQ ETF and a nearly 56% weight in the DIA ETF.

Drivers of Performance: A fund’s performance is largely determined by both the selection and sizing of positions in a portfolio. Selection is intuitive: Are the right stocks being chosen in a portfolio to deliver returns? Additionally, a larger percentage weight in a portfolio implies a higher position size in the portfolio.

Position Size & Position Performance

The following 2 charts illustrate the position size (% weight) & position performance (% return) of the underlying stocks in QQQ and DIA:

___

Key Insights (data from Koyfin, as of November 1, 2022):

Dispersion: The year-to-date (YTD) percentage price changes have larger dispersion and a wider range in the underlying stocks within QQQ compared to the underlying stocks within DIA.

Position Weight: UnitedHealth Group (UNH) has the largest percentage weight in DIA (about 11.2%), while Apple (AAPL) has the largest percentage weight in QQQ (about 14.2%).

Underlying Portfolio Company Price Change Profile for DIA ETF:

YTD, the 3 highest stock price return movers within the DIA ETF are Chevron (CVX), Merck (MRK), and Amgen (AMGN).

YTD, the 3 worst stock price returns within the DIA ETF are Intel (INTC), Nike (NKE), and Salesforce (CRM).

Underlying Portfolio Company Price Change Profile for QQQ ETF:

YTD, the 3 highest stock price return movers within the QQQ ETF are Vertex Pharmaceuticals (VRTX), T-Mobile US (TMUS), and Amgen (AMGN).

YTD, the 3 worst stock price returns within the QQQ ETF are Okta (OKTA), Meta Platforms (META), and Align Technology (ALGN).

References:

NASDAQ 100 Index Methodology, Nasdaq, Accessed 10/28/2022, https://indexes.nasdaq.com/docs/Methodology_NDX.pdf

Dow Jones Industrial Average, S&P Dow Jones Indices, S&P Global, Accessed 10/28/2022, https://www.spglobal.com/spdji/en/indices/equity/dow-jones-industrial-average/#data

“There Are Now More Indexes Than Stocks”, Bloomberg News, Published on 5/12/2017, https://www.bloomberg.com/news/articles/2017-05-12/there-are-now-more-indexes-than-stocks

Koyfin, https://www.koyfin.com/home

DIA ETF, Morningstar, Accessed 10/28/2022, https://www.morningstar.com/etfs/arcx/dia/portfolio

QQQ ETF, Morningstar, Accessed 10/28/2022, https://www.morningstar.com/etfs/xnas/qqq/portfolio

This letter is not an offer to sell securities of any investment fund or a solicitation of offers to buy any such securities. An investment in any strategy, including the strategy described herein, involves a high degree of risk. Past performance of these strategies is not necessarily indicative of future results. There is the possibility of loss and all investment involves risk including the loss of principal.

Any projections, forecasts and estimates contained in this document are necessarily speculative in nature and are based upon certain assumptions. In addition, matters they describe are subject to known (and unknown) risks, uncertainties and other unpredictable factors, many of which are beyond Drawing Capital’s control. No representations or warranties are made as to the accuracy of such forward-looking statements. It can be expected that some or all of such forward-looking assumptions will not materialize or will vary significantly from actual results. Drawing Capital has no obligation to update, modify or amend this letter or to otherwise notify a reader thereof in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate.

This letter may not be reproduced in whole or in part without the express consent of Drawing Capital Group, LLC (“Drawing Capital”). The information in this letter was prepared by Drawing Capital and is believed by the Drawing Capital to be reliable and has been obtained from sources believed to be reliable. Drawing Capital makes no representation as to the accuracy or completeness of such information. Opinions, estimates and projections in this letter constitute the current judgment of Drawing Capital and are subject to change without notice.