Index Funds Impact Price Volatility & Change Market Structure

Weekly updates on the innovation economy.

Today’s newsletter focuses on a series of non-consensus and contrarian insights in how the rise of passive index fund investing is impacting price volatility and changing market structure.

Positive Benefits of Index Funds

The rise of index funds has overwhelmingly been a net positive for individual investors, and benefits include the following:

Lower fees for investors

Greater access to diversified investment vehicles

Ability to easily track popular market indices or themes

Improved tax efficiency with buying-and-holding 1 index fund as opposed to frequently buying-and-selling stocks (which can create capital gains taxes)

Time efficiency and reduced investment complexity with buying 1 S&P 500 index fund instead of buying and managing 500 individual stocks

Contrarian and Non-Consensus Insights About Index Funds Impacting Price Volatility and Market Structure

Nonetheless and even with these positive benefits associated with index funds, we believe that it is also important to note the acknowledgements listed below to understand how the rise in passive index fund investing is impacting price volatility and changing market structure, which impacts all investors. These acknowledgements and insights include the following:

Fund flows, not valuation, are increasingly a determining factor for market returns as passive & index investing increases relative to active management. Passive index investing is a simple algorithm, and when an index fund receives more money from investors, a broad-based stock market index fund automatically buys more of the underlying investments in the index without any regard to a company’s valuation, earnings power, quality of products, diversity initiatives, environmental sustainability goals, or other parameters.

While many people perceive active portfolio management as an industry that is paid to value securities, this perception is somewhat incorrect. The reality is that active fund managers are paid to do research on securities in order to provide liquidity to the market. If Investor X wants to sell a stock to someone else at a really low price relative to their research and estimations, then someone else is willing to buy shares from Investor X in order to participate in the investment’s potential upside, thereby providing liquidity to the market in exchange for receiving a potential future return on investment.

Providing liquidity implies giving someone cash in exchange for an asset. Taking liquidity is selling an investment in return for cash. When the Federal Reserve implements a quantitative easing monetary policy, the Federal Reserve is buying billions of dollars of securities every month, thereby providing liquidity (via cash) to financial market participants.

As a greater share of the equity market is invested via passive index funds, closet indexers, and algorithmic-based quantitative investors, there is a proportionately less market share of active managers that can readily provide and take liquidity. As a result, it’s increasingly common to see significant price fluctuations in indices on volatile market trading days. In Q1 2020 and with the outbreak of the coronavirus, major stock market indices witnessed some of the largest one-day price drops in history, and significant selling cascaded into more selling.

According to a Bloomberg article published in May 2020, “The average intraday move for S&P 500 stocks after earnings is the highest on record since 2009, according to analysis from Goldman Sachs.” Additionally, there is rising volatility when large business fundamental events are occurring, such as on the dates of corporate earnings releases.

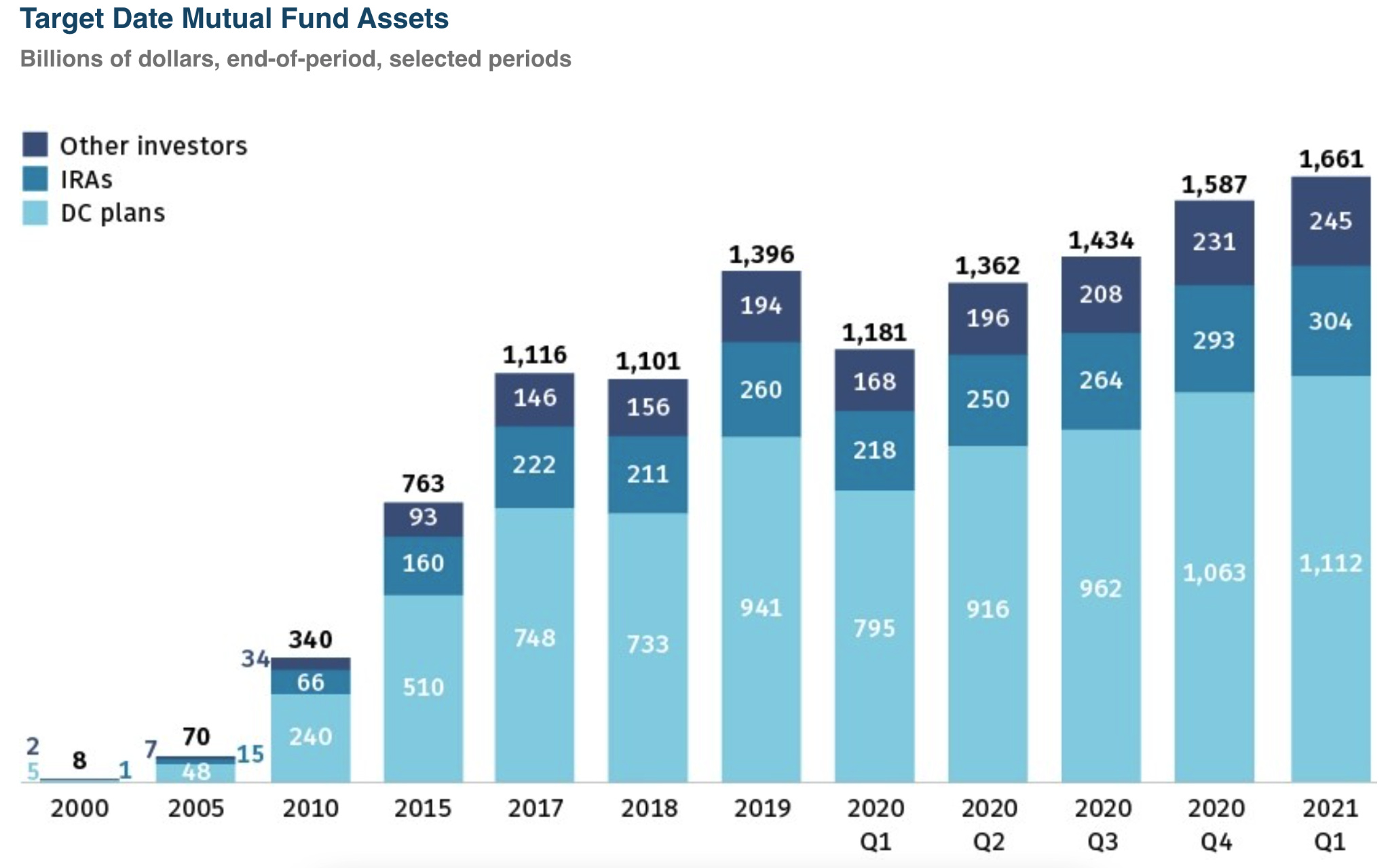

Financial Assets in Retirement Accounts

One narrative is that as the size of retirement assets increase from ongoing retirement plan contributions and growth in the value of assets (particularly in 401k plans that are largely invested in target date funds or index funds), trillions of dollars are being blindly invested into the market without any regard to valuation, product quality, consumer satisfaction, financial margins, corporate earnings power, or other parameters.

_

_

Market Structure for S&P 500 Index is Changing

Interestingly and despite the free-fall in financial asset prices in Q1 2020, the percentage chance of downside risk for S&P 500 index funds has been reduced under the tenure of Federal Reserve Board Chairman Jay Powell. When there is less perceived risk in financial markets, then asset prices increase. We can see this via the following chart below for the SPDR S&P 500 ETF (which seeks to track the performance of the S&P 500 Index under ticker symbol: SPY).

Expansionary monetary policy leads to higher market liquidity (which can reduce volatility), and lower uncertainty with lower interest rates incentivize investors to pay higher prices for stocks, bonds, real estate, and other financial assets. Furthermore, it is increasingly clear that the Federal Reserve pays close attention to the health of financial markets and their stability.

Concluding Thoughts

Even with the tremendous positive benefits associated with index funds, we believe that it is also important to acknowledge and understand how the rise in passive index fund investing and the Federal Reserve’s monetary policy are impacting price volatility and changing market structure.

Ultimately, understanding market structure, historical outcomes, and a changing investing landscape can help more investors get the odds of investing success in their favor.

References:

Ro, Sam. “S&P 500 Index Funds Balloon.” Axios, Axios, 7 July 2021, www.axios.com/sp-500-index-funds-record-50975ba0-1ef5-4d70-a14b-ea01a1a9ed3e.html. Accessed 18 Oct. 2021.

Calderone, Gregory. “Earnings-Day Price Moves Are the Largest since ‘09, Goldman Says.” Bloomberg, 12 May 2020, www.bloomberg.com/news/articles/2020-05-12/earnings-day-price-moves-are-the-largest-since-09-goldman-says. Accessed 18 Oct. 2021.

“Annual Survey of Assets as of December 31, 2020.” S&P Global, Inc. https://www.spglobal.com/spdji/en/documents/index-news-and-announcements/spdji-indexed-asset-survey-2020.pdf. Accessed 18 Oct. 2021.

"Koyfin | Advanced graphing and analytical tools for investors." https://app.koyfin.com/. Accessed 17 October. 2021.

“Retirement Assets Total $37.2 Trillion in Second Quarter 2021.” Investment Company Institute (ICI), 29 Sept. 2021, www.ici.org/statistical-report/ret_21_q2. Accessed 18 Oct. 2021.

This letter is not an offer to sell securities of any investment fund or a solicitation of offers to buy any such securities. An investment in any strategy, including the strategy described herein, involves a high degree of risk. Past performance of these strategies is not necessarily indicative of future results. There is the possibility of loss and all investment involves risk including the loss of principal.

Any projections, forecasts and estimates contained in this document are necessarily speculative in nature and are based upon certain assumptions. In addition, matters they describe are subject to known (and unknown) risks, uncertainties and other unpredictable factors, many of which are beyond Drawing Capital’s control. No representations or warranties are made as to the accuracy of such forward-looking statements. It can be expected that some or all of such forward-looking assumptions will not materialize or will vary significantly from actual results. Drawing Capital has no obligation to update, modify or amend this letter or to otherwise notify a reader thereof in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate.

This letter may not be reproduced in whole or in part without the express consent of Drawing Capital Group, LLC (“Drawing Capital”). The information in this letter was prepared by Drawing Capital and is believed by the Drawing Capital to be reliable and has been obtained from sources believed to be reliable. Drawing Capital makes no representation as to the accuracy or completeness of such information. Opinions, estimates and projections in this letter constitute the current judgment of Drawing Capital and are subject to change without notice.