In today’s Drawing Capital newsletter, we explore the concept of unbundling complexity into simplicity to directly translate into generating investment returns.

3 topics of emphasis in today’s newsletter include:

Occasionally, the simplest investing ideas can create enormous wealth.

We explore the popular reasons on why simple investing ideas are difficult to follow in real life.

Riding a sustainably growing multi-billion dollar tailwind or finding a non-obvious insight can both be incredibly valuable from an investment perspective.

Why are simple investing ideas occasionally difficult to follow in real life?

A juxtaposition of consensus thinking and performance alpha: If an idea is so simple, some investors assume that the idea is common knowledge and therefore has little investing alpha above a benchmark index, thereby influencing the decision not to invest.

Bias towards action: Many investors and traders feel the need (quantitatively or behaviorally) to frequently rebalance a portfolio and try several different strategies instead of being patient in remaining committed to a singular strategy for an extended period of time.

Doubt and investing anxiety: How can something so simple actually work out well? Am I thinking of this incorrectly or without proper analysis?

Misalignment of incentives: Some money managers are unfortunately incentivized to demonstrate perpetual motion on making frequent portfolio changes, regardless if they are major or minor in consequence. It is important to not lose sight of an important lesson: The purpose of investing is to promote financial wellness and generate better outcomes.

Price anchoring bias: For example, a stock that was previously at $85 just became $200 last year, and now it’s trading at $300. An investor with price anchoring bias may feel that they missed out on the majority of investment gains or are buying at high prices due to previous price anchoring, thereby influencing a decision to not invest.

A quick note: Obviously, not all “simple” investing ideas become winners, and future performance often deviates from historical returns.

With hindsight bias, here are 7 examples of “simple” investing ideas that would have generated significant returns:

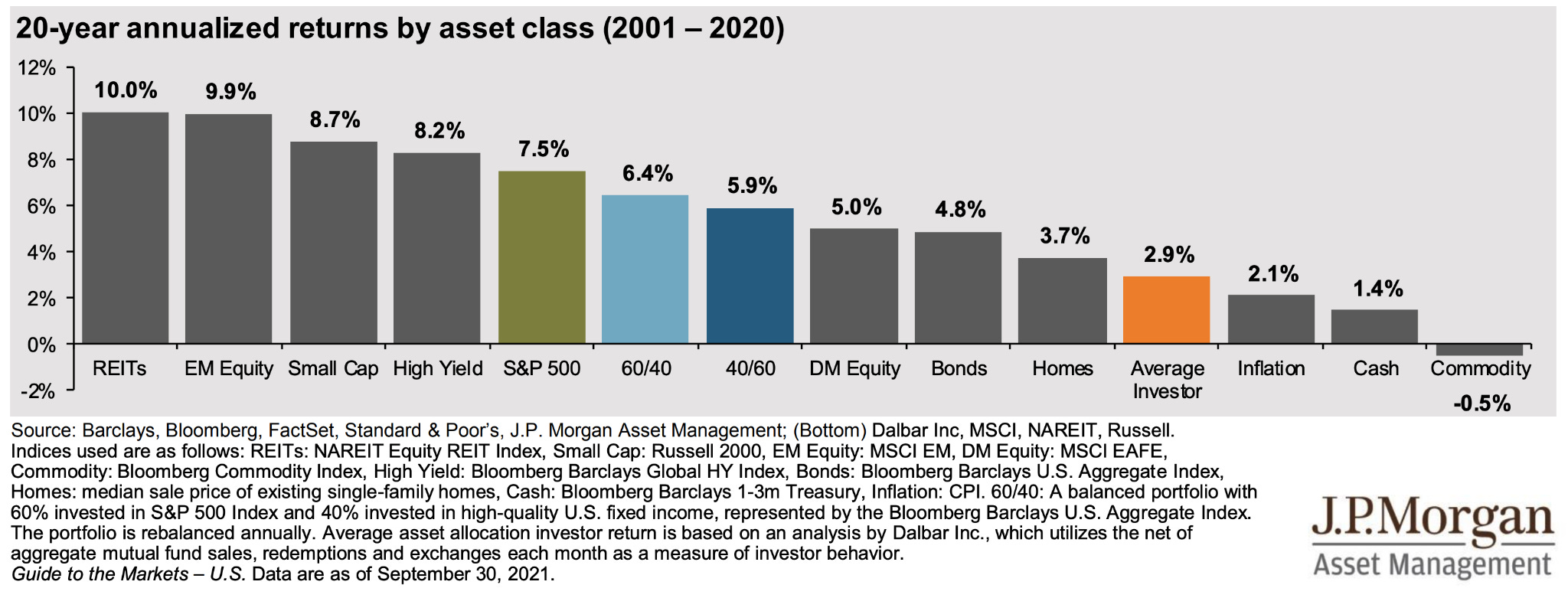

Buying a low-cost, high-quality S&P 500 index fund without any individual company-specific research and holding the investment for decades would have generated better returns than the average investor, been tax-efficient (due to limited trading decisions that would have otherwise created capital gains taxes), and generated significant positive returns.

The chart from J.P. Morgan below highlights the annualized returns by asset class from 2001-2020. A surprising conclusion from this chart is that the average investor is generating investment returns that just marginally exceeds the inflation rate.

Looking at this dashboard from S&P Global, the overwhelming majority of large-cap actively managed mutual funds underperformed the S&P 500 Index over the past decade:

From 2013-2020, the collective market caps of these Big Tech “FANGMAN” companies grew about ~7x, or about a ~28% compounded annual growth rate. The “FANGMAN” acronym stands for Facebook, Apple, Netflix, Google (or Alphabet), Microsoft, Amazon, and NVIDIA. A 7x increase between 2013-2020 would have performed better than the S&P 500 Index, the NASDAQ index, the realized gains across many venture capital funds, and almost all Fidelity funds.

After the early beginnings of the coronavirus crisis, the Federal Reserve enacted unprecedented monetary policy through a combination of low interest rates, expansion of the Federal Reserve’s balance sheet, rapid increase in M2 money supply (aka “money creation”), quantitative easing with significant financial asset purchasing, involvement in the corporate bond market, and more. From Q2 2020-Q2 2021, this flood of trillions of money creation and capital started inflating the prices of several asset prices, particularly in asset classes with limited supply, such as Bitcoin, gold, real estate, NFTs, art, high-growth software stocks, and more.

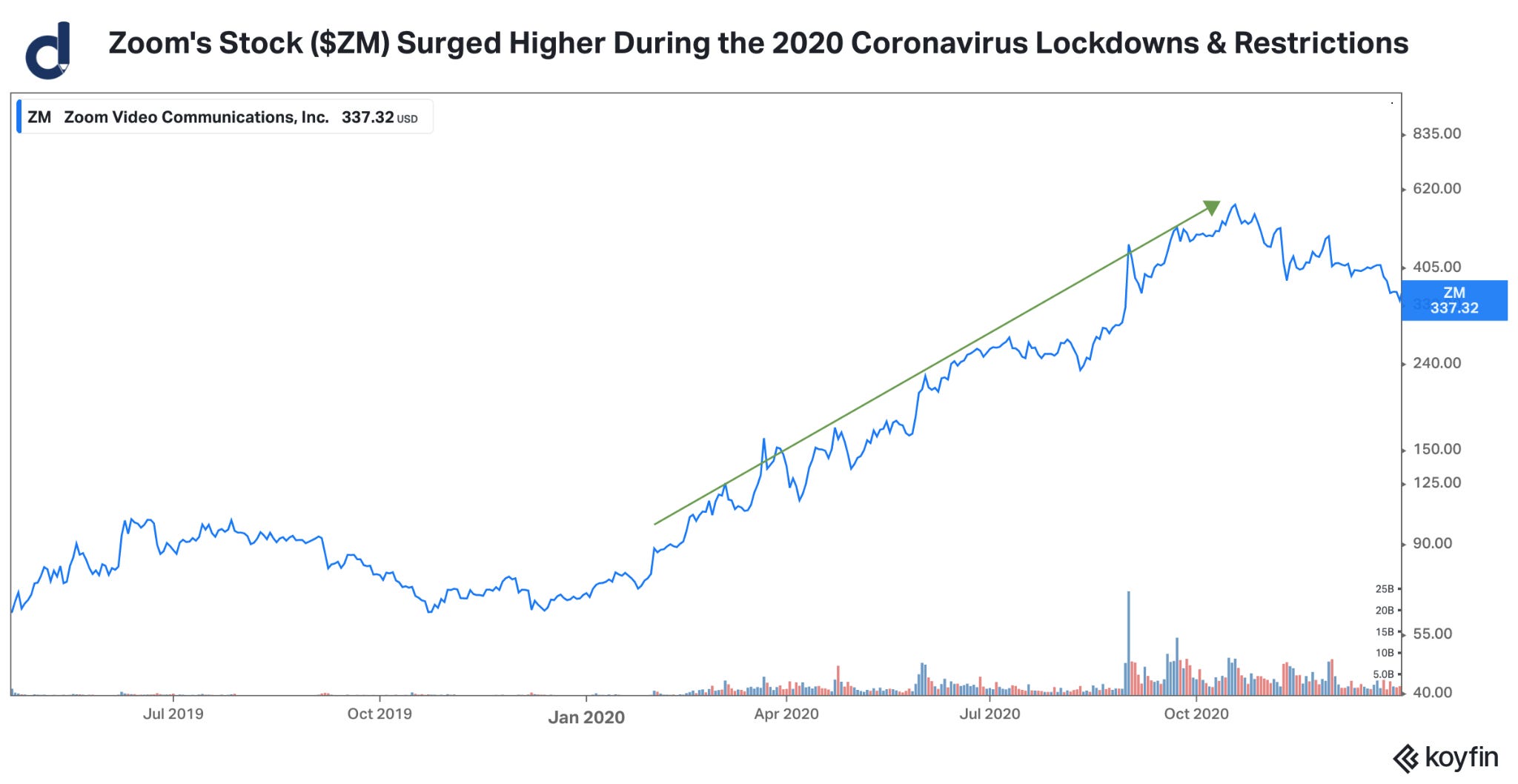

After the early beginnings of the coronavirus crisis and after several announcements from thousands of companies about a work-from-home policy to comply with lockdown notices, an obvious method of conducting meetings virtually was through Zoom. In 2020, Zoom’s stock price skyrocketed, as seen by the chart below:

If an investor has high confidence in forecasting commodity prices such as gold or oil, then buying a basket of gold miners or oil producers in anticipation of rising gold and oil prices has historically been lucrative.

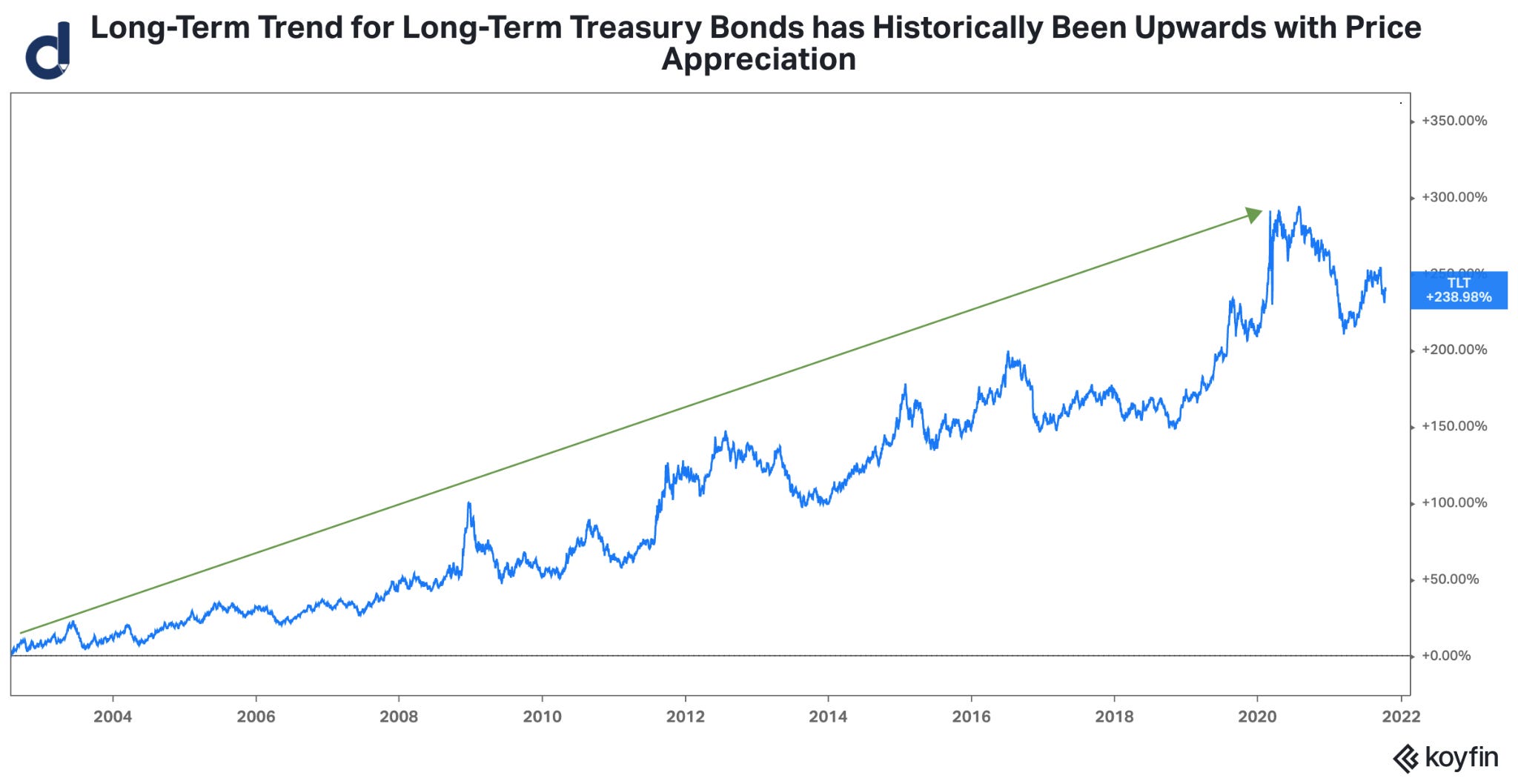

Buying and holding 30-year Treasury bonds, especially when purchased at high yield-to-maturities (YTM), have performed well over the years. As interest rates have enjoyed a (more or less) long-term downward trend since 1982, bond prices have performed well during this 40-year bond bull market.

Being a supporter of diversity, inclusion, and equality initiatives has both been morally correct and positively profitable.

In aggregate, buying the companies that promote equality promotes employees feeling empowered to contribute more, feeling a sense of relative fairness, and achieving historically better returns for shareholders.

As per Dr. Dan Ariely’s research, “If we take our data set from 2006, and every year we calculate which companies are the ones that are treating their women most equal to men. And we buy the top 20% of companies every year who are doing that. And we construct a portfolio like this, that portfolio has a return of about 5.4% a year above the S&P — just adjust by looking at equality, nothing else.” (Source: Bloomberg Odd Lots Interview with Dr. Dan Ariely in June 2021).

Concluding Thoughts

The role of this newsletter post helps to demonstrate that occasionally, the simplest investing ideas can work out well to generate returns.

One of the most important traits in investing is focus. It is difficult to perform well in every asset class for extended periods of time, and instead, many successful investors often specialize in one area and do it well. The lesson here is that narrowing the focus can elevate the level of excellence.

While the above examples demonstrate samples of “simple” investing ideas that would have performed well with hindsight bias, investing has risks, is a hyper-competitive industry, and evolves over time. Top-tier investment firms with deep research expertise, ability to produce compelling insights, and capability to generate attractive returns to their investors provide tremendous value.

Change creates opportunities. The best winning investments of yesterday may not necessarily be the best winning investments of the future. Technological advancement and innovation enable exceptional startups and thriving companies with moats to amplify their competitive advantages.

There are four necessary skills in investing, in this order:

1) Sourcing Investments: How does one find investment opportunities and ideas?

2) Analysis: How does one analyze companies, industry trends, and asset classes?

3) Insight: After sourcing and analysis, what are the couple of key insights that drive an investment’s possible distribution of outcomes? Synthesizing through the dozens and hundreds of pages of analysis, what matters most, and why?

4) Judgement: Does a potential investment make it into a portfolio? What is the level of conviction and confidence in the investment? What is the investment’s percentage weight in the portfolio? How will the investment inside a portfolio be managed over time?

“SPIVA | S&P Dow Jones Indices.” www.spglobal.com, www.spglobal.com/spdji/en/research-insights/spiva/#/reports. Accessed 18 October 2021.

"Koyfin | Advanced graphing and analytical tools for investors." https://app.koyfin.com/. Accessed 17 October. 2021.

This letter is not an offer to sell securities of any investment fund or a solicitation of offers to buy any such securities. An investment in any strategy, including the strategy described herein, involves a high degree of risk. Past performance of these strategies is not necessarily indicative of future results. There is the possibility of loss and all investment involves risk including the loss of principal.

Any projections, forecasts and estimates contained in this document are necessarily speculative in nature and are based upon certain assumptions. In addition, matters they describe are subject to known (and unknown) risks, uncertainties and other unpredictable factors, many of which are beyond Drawing Capital’s control. No representations or warranties are made as to the accuracy of such forward-looking statements. It can be expected that some or all of such forward-looking assumptions will not materialize or will vary significantly from actual results. Drawing Capital has no obligation to update, modify or amend this letter or to otherwise notify a reader thereof in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate.

This letter may not be reproduced in whole or in part without the express consent of Drawing Capital Group, LLC (“Drawing Capital”). The information in this letter was prepared by Drawing Capital and is believed by the Drawing Capital to be reliable and has been obtained from sources believed to be reliable. Drawing Capital makes no representation as to the accuracy or completeness of such information. Opinions, estimates and projections in this letter constitute the current judgment of Drawing Capital and are subject to change without notice.