SPAC Analysis for Social Capital Hedosophia Holdings

Weekly updates on the innovation economy.

Drawing Capital Newsletter

February 4, 2021

Introduction

As a bonus edition for Drawing Capital’s weekly newsletter, we are excited about discussing the current SPAC landscape and investing opportunities in SPACs. For a review of Drawing Capital’s recent thoughts on the IPO and SPAC market, please view our recent webinar presentation at the following link:

Why Are SPACs Popular?

The first question that is often asked by investors is, “Why now for the SPAC movement?” We believe these are the 4 key reasons why SPACs have become popular now.

There exists a constrained supply of enduring high-growth and high-quality companies in public markets. Investors increasingly are seeking high-return and growth-focused strategies in a low-interest-rate environment.

Company executives increasingly prefer faster speed-to-market, better valuation certainty, and less dilution as top preferences in the process of going public.

The success of some SPACs have re-legitimized the SPAC transaction process. A SPAC sponsor with deep financial market sophistication, operational and technical expertise, and the ability to bring venture-capital-like hyper-scaling abilities to companies adds value and reduces the dual principal-agent problem.

There is improved guidance and transparency to investors. When investing in innovative technologies, it is important to focus on future returns and future progress, not the past, especially since the majority of the current value of a technology company is based on its future plans, ideas, technologies, and cash flows. A SPAC transaction allows a discussion on forecasts, while the IPO process has restricted ability to make forward-looking predictions.

Risks in SPACs

Despite the rising popularity of SPACs, several key risks remain:

A successful SPAC transaction is highly dependent on both the quality of the private company going public and the quality of the SPAC sponsor. A lack of quality in either or both of these parties can possibly lead to suboptimal outcomes or investment losses.

The typical $10/share redemption feature goes away after the completion of taking the private company public, thereby adding downside risk to an investment.

SPAC shareholders can suffer from equity dilution, thereby depressing a stock price.

The composition of SPAC shareholders often changes after the completion of taking a private company public via a SPAC process. Said differently, many SPAC shareholders exit their investment after the announcement of a target private company to take public via a SPAC.

After a private company goes public via a SPAC, its future stock price is based on the company’s fundamentals, future cash flows, price multiples, investor sentiment, and other factors.

In the event that a SPAC sponsor does not find a target private company to merge with within 2 years, the SPAC shareholder may receive a trivial return (if SPAC shares were purchased at the SPAC launch issuing price) or a loss (if SPAC shares were purchased above the SPAC launch issuing price, which is typically $10/share).

Many private companies with speculative technologies and speculative future projections are approaching the SPAC market to take advantage of the trend, thereby giving a wide dispersion of quality across various SPACs.

Many SPAC transactions have less due diligence compared to many IPOs.

Given both the significant volume of SPAC launches and the dollars fundraised in SPACs, many SPAC sponsors are chasing the same set of private companies, thereby driving up late-stage private company valuations. Multiple SPAC sponsors are increasingly competing against each other to take a specific private company to the public equity markets.

Like many investments, SPACs have no bank guarantee, are not FDIC insured, and may lose value. SPACs have investment risks.

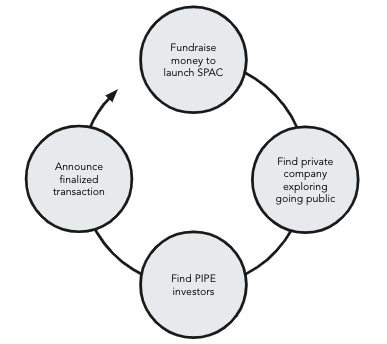

The SPAC Process

As displayed in the above diagram, these are the following key steps in the SPAC process from the perspective of a SPAC sponsor:

Step 1 is to fundraise money and launch a SPAC on a stock exchange with the intent of acquiring an ownership interest in a private company.

Step 2 is to find compelling private companies in the “going public” exploration stage in an effort to take a company public.

Step 3 is to find PIPE (Private Investment in a Public Entity) investors.

Step 4 is to announce, merge, and finalize a SPAC transaction with a private company that is seeking to go public on a listed stock exchange.

Surging SPAC Trend

As we can see from the above chart, 2020 experienced a record surge in the amount of SPAC launches.

The average size of a SPAC launch has been steadily increasing since 2009, allowing for a wider array of companies that can go public via a SPAC.

2020 was a year in which both the number of SPAC launches and the average size of a SPAC launch reached record highs.

Furthermore, tens of billions of dollars are chasing private companies to target a public listing via a SPAC transaction.

In summary, there are a number of key benefits for multiple parties that participate in the SPAC ecosystem:

Private companies benefit from the ability to go public with speed, greater certainty, and a strategic partnership with a SPAC sponsor.

From a SPAC sponsor’s perspective, the SPAC sponsor becomes an investor in a late-stage private company that it likes, the SPAC sponsor often receives significant upside via a “promote”, and the SPAC capital fundraising process is easier when there is lots of popularity and interest in SPACs.

From the perspective of public market investors in SPACs, benefits include the ability for public market investors to participate in the growth of private companies when they become public and beyond and the ability to redeem shares prior to the formal completion of a SPAC deal, thereby providing an interesting risk/reward opportunity.

Investing Opportunities in SPACs

From the perspective of a SPAC investor and shareholder, there are two common investing strategies for seeking opportunities in SPACs: a growth strategy and a recurring return strategy.

From a growth strategy perspective, an investor can seek out high-quality SPAC sponsors that will hopefully pursue really interesting private companies to take public. During this process, the investor can fundamentally understand a company’s business model, forward-looking growth prospects, existing technology, investor sentiment, and much more before the closure of a SPAC deal with a private company. In the event that a SPAC investor does not like the private company being taken public, the SPAC sponsor can utilize the redemption feature.

From a recurring return strategy perspective, the goal here is to generate frequent positive returns by capitalizing on the delta between the SPAC launch price, which is typically at $10 per share, and the SPAC’s current market price. Of course, the hope is that the winners exceed the losing investments. As market enthusiasm for a SPAC increases, the SPAC’s stock price typically increases as well. Running this strategy across a basket of SPACs could potentially provide a diversified source of return that can exceed current bond market returns with little correlation to broad market equity indices.

In summary, both a growth strategy and a recurring return strategy for SPACs provide an interesting investment opportunity set.

SPAC Analysis for Social Capital Hedosophia Holdings

Finally, we would like to highlight a case study for Social Capital Hedosophia Holdings, which is a popular SPAC sponsor within the SPAC ecosystem. This team tends to focus on disruptive technologies and innovation across a range of themes. For example:

IPOA merged with Virgin Galactic ($SPCE), a space tourism company.

IPOB merged with OpenDoor ($OPEN), a fintech company that is revolutionizing consumer real estate purchases and online property transactions.

IPOC merged with Clover Health ($CLOV), a health insurance company that aims to lower costs and deliver better outcomes through data science and a technology-enabled approach.

IPOE recently announced a merger with SoFi ($IPOE), a fintech company seeking to disrupt the traditional consumer banking and financial services model in an effort to craft better consumer experiences.

In addition to these SPACs, Social Capital CEO Chamath Palihapitiya has participated in a variety of PIPEs in private companies that are going public via a SPAC transaction, including publicly-announced PIPE investments in the following:

Desktop Metal ($DM), a 3D printing company with a focus on additive manufacturing

Metromile ($INAQ), a company that focuses on risk pricing and car insurance through a data science platform with usage-based pricing

MP Materials ($MP), a mining company that mines for essential rare Earth minerals that power the vehicle electrification movement, reduce carbon emissions, and contribute to other technological applications

Proterra ($ACTC), an electric bus manufacturing company

Sunlight Financial ($SPRQ), a residential point-of-sale solar financing company

Latch ($TSIA), a smart-lock and smart-home device provider and an enterprise SaaS company in the real estate industry

In terms of the SPAC movement, Social Capital CEO Chamath Palihapitiya has certainly gained investor and media fanfare and provided leadership to the Silicon Valley ecosystem. Mr. Palihapitiya’s successful IPOA & Virgin Galactic SPAC transaction provided validation to his “IPO 2.0 Movement” and triggered a wave of new SPAC transactions. Mr. Palihapitiya has reserved NYSE ticker symbols IPOA through IPOZ, indicating that Social Capital Hedosophia Holdings intends to sponsor at least 26 SPAC transactions. He is also exploring a SPAC platform for biotech companies.

Importantly, we feel that the quality of a SPAC sponsor is very important. A SPAC sponsor is an individual or entity that connects with a private company in order to take the private company public via a SPAC transaction. We feel that a high-quality SPAC sponsor embodies the following 4 traits:

Operational and technical excellence

Financial market sophistication

Material personal investment from a SPAC sponsor to demonstrate alignment of financial interests between the SPAC sponsor, SPAC shareholders, and the private company being taken public via a SPAC

Ability to connect with other high-quality investors for a private investment in public equity (PIPE) during the SPAC process

Reviewing Mr. Palihapitiya’s recent SPAC transactions and PIPE deals, one can deduce a list of implied parameters that Mr. Palihapitiya seeks when evaluating SPAC transactions:

Look for companies that satisfy one or more of the following 10 themes:

E-commerce and online consumption

“Deep-tech” and hard technologies

Healthcare, health IT, and digital therapeutics

Sustainability, climate change, and decarbonization

Fintech

Artificial intelligence and machine learning

Enterprise SaaS

Consumer network effects and subscription services

Education

Biotech

Find large markets with a significant incumbent-dominated market. Often, these incumbent-dominated markets have mediocre or low customer satisfaction scores and inadequate technological progress. Example markets include healthcare, education, space travel & tourism, residential real estate, decarbonization, financial services, manufacturing, and other industries.

Look at companies with reasonable valuations: forward projected EV/revenue ratios and other price multiples should be modest, nor exorbitant.

Look for a virtuous cycle with potential future flywheel effects beyond a core business model so that the company can continue to grow its revenue and increase its total addressable market.

Look to leverage technology, data science, and operating expertise to scale businesses.

Look for disruptive technologies that enable durable moats in businesses. These types of technologies enhance consumer experiences, can decrease costs, can increase the speed of delivery to consumers and enterprises, and questions an incumbent company’s legacy business model.

Look for a “margin of valuation safety” based on both modest valuation multiples and strong underlying industry tailwinds.

Focus on companies and technologies that have the asymmetric potential to provide transformative experiences, advance humanity forward, and solve hard problems.

Look to partner with high-quality management teams.

Democratize investor access, promote financial inclusion, and improve liquidity by allowing public market investors to finance and invest in the long-term growth of iconic technology companies.

Avoid companies that spend the vast majority of their revenues on large customer acquisition costs through advertising on Google and Facebook.

Avoid companies that do not have strong projected future revenue growth rates.

Build a portfolio of companies with the possibility of generating 10X return in 10 years.

The summation of the above factors provides high conviction to warrant a minimum investment of $100M of his personal money. There is a greater alignment of interests when the SPAC sponsor acts as a “principal” rather than as an “agent”.

Conclusion

The decision for a company to seek a public listing of its shares on a stock exchange represents an important milestone in a company’s journey. The recent rise in direct listings and SPACs as formidable alternatives to the traditional IPO process demonstrates the growing need for enhanced transparency, efficiency, prioritization of goals, and stakeholder management. Understanding SPACs and notable SPAC sponsors can expand an investor’s knowledge and opportunity set.

Get in touch to learn more about Drawing Capital’s strategy:

References:

(1) Drawing Capital & Interactive Brokers. “Drawing Capital- IPOs and SPACs: The Next Evolution of Going Public”. 25 Jan 2021.

(2) "SPAC Data." https://spacdata.com/. Accessed 25 Jan. 2021.

(3) "SPAC Analytics - Home." https://www.spacanalytics.com/. Accessed 25 Jan. 2021.

(4) "SPAC IPO Transactions Statistics - by SPACInsider." https://spacinsider.com/stats/. Accessed 25 Jan. 2021.

(5) "SPACs Could Become Formidable Bidders in the M&A Market ...." https://www.debevoise.com/insights/publications/2020/12/spacs-could-become-formidable-bidders. Accessed 25 Jan. 2021.

(6) Corporate press releases from Virgin Galactic, OpenDoor, Clover Health, and SoFi

(7) "Social Capital (@socialcapital) | Twitter." https://twitter.com/socialcapital. Accessed 25 Jan. 2021.

(8) "Chamath Palihapitiya (@chamath) | Twitter." https://twitter.com/chamath. Accessed 25 Jan. 2021.

(9) "Sway: At-Home Covid Tests and Other Powers of a Tech Billionaire ...." https://podcasts.apple.com/us/podcast/at-home-covid-tests-and-other-powers-of-a-tech-billionaire/id1528594034?i=1000498757332. Accessed 2 Feb. 2021.

This letter may not be reproduced in whole or in part without the express consent of Drawing Capital Group, LLC (“Drawing Capital”).

This letter is not an offer to sell securities of any investment fund or a solicitation of offers to buy any such securities. An investment in any strategy, including the strategy described herein, involves a high degree of risk. Past performance of these strategies is not necessarily indicative of future results. There is the possibility of loss and all investment involves risk including the loss of principal.

The information in this letter was prepared by Drawing Capital and is believed by the Drawing Capital to be reliable and has been obtained from sources believed to be reliable. Drawing Capital makes no representation as to the accuracy or completeness of such information. Opinions, estimates and projections in this letter constitute the current judgment of Drawing Capital and are subject to change without notice.

Any projections, forecasts and estimates contained in this document are necessarily speculative in nature and are based upon certain assumptions. In addition, matters they describe are subject to known (and unknown) risks, uncertainties and other unpredictable factors, many of which are beyond Drawing Capital’s control. No representations or warranties are made as to the accuracy of such forward-looking statements. It can be expected that some or all of such forward-looking assumptions will not materialize or will vary significantly from actual results. Drawing Capital has no obligation to update, modify or amend this letter or to otherwise notify a reader thereof in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate.