Wealthy Software Engineers Are Implicitly Good Stock Pickers

Weekly updates on the innovation economy.

Introduction

In today’s newsletter, we explore the following 3 topics:

Financialization of compensation, particularly for software engineers, several tech employees, and company executives

Historical returns from software investing and growth in “Big Tech” companies

Understanding how software engineers, tech employees, and employees with stock-based compensation can potentially personally increase their total pay with the financialization of RSUs.

Important Software Metrics

Software investing is growth investing, and as a result, most startups and publicly traded software & cloud companies are valued based on their revenue, future revenue growth rates, durability of future revenue growth rates, margins, free cash flow, and other metrics. Additionally, qualitative factors such as product quality and paths to positive profitability, among other factors, are relevant for further evaluation for analyzing software companies among founders, employees, investors, and key customers.

Ultimately, how can you increase the value of your software company?

In a previous Drawing Capital blog post, we highlighted 12 popular software metrics that are useful for either investors, founders, and builders of software companies. This post can be found here:

Multiplying Money via Compounding Returns

CAGR = compounded annualized growth rate

MOIC = multiple on invested capital

Key Takeaway: There is a positive relationship between higher CAGR and higher MOIC. From a “working backwards” perspective by first identifying the goal and then creating a roadmap to achieving the goal, if an investor desires a 10x investment return in the next 10 years, this goal implies a nearly 26% CAGR.

Historical Returns From Investing in Software

Over the past decade, several technology & software index funds have both performed positively and performed better than the S&P 500 Index, which is among the most popular benchmark indices for tracking the performance of American large-cap stocks.

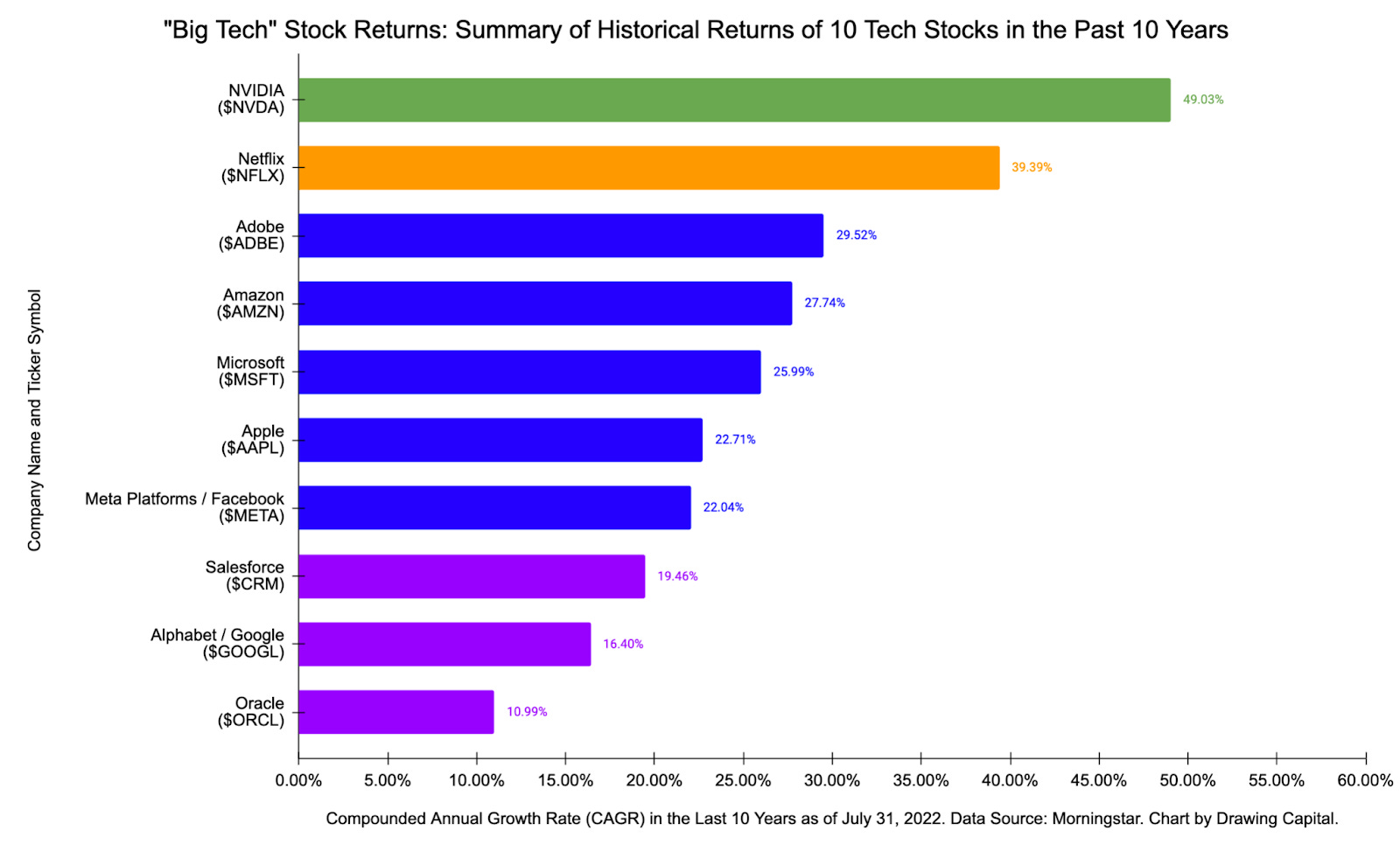

Now, let's take a look at ten historical “Big Tech” stock returns for the past 10 years as of July 31, 2022. As illustrated in the chart below, “Big Tech” companies have delivered significant returns to shareholders and stock-owning employees:

Additionally, the following chart illustrates the significant size and growth of these 10 “Big Tech” companies:

Key Insights:

The size, scale, and scope of “Big Tech” companies are significant. As of August 1, 2022, the cumulative market cap values of these 10 “Big Tech” companies exceeded $9 trillion.

From 2012 to 2021, the end-of-year cumulative market cap values of these 10 “Big Tech” companies always increased.

From 12/31/2012 to 12/31/2021, the cumulative market cap values of these 10 “Big Tech” companies increased by more than 8.8x.

From 12/31/2012 to 8/1/2022, NVIDIA had the largest multiplier increase in market cap, moving from about $7.7 billion to about $462 billion in market cap. When measured in dollar value across the same time range, Apple created $2.1 trillion in market cap and Microsoft created $1.85 trillion in market cap.

Apple’s market cap on 8/1/2022 (nearly $2.6 trillion) exceeded the cumulative market cap values of these 10 “Big Tech” companies on 12/31/2015.

Are Software Engineers and Employees with Stock-Based Compensation Implicitly Stock Pickers?

Now that we have a foundation and a perspective about historical software index returns and the growth of “Big Tech” companies, we can explore the following question: Are software engineers and employees with stock-based compensation implicitly stock pickers?

Examples of stock-based compensation include RSUs and employee stock options. High use of stock-based compensation broadens shareholder ownership, conserves corporate cash flow, and allows employees to participate in the potential growth of their employer’s stock price.

Engineers and tech employees that build significant wealth are implicitly good stock pickers. Why? Since software engineers have typical 4-year vesting schedules for RSUs, a software engineer’s total compensation during the employment time period for a company is based on 3 factors:

Starting position level (i.e. IC Level 4, 5, 6, etc.)

Employer’s and manager’s perceived quality of an employee’s work (i.e. performance reviews, promotions, bonuses, stock refresher grants, salary increases, etc.)

Growth in the employer’s stock price

Since significant wealth can be often earned via stock ownership of publicly-traded and/or private companies (i.e. owning equity [shares] in a company), choosing to work at high-growth companies can potentially generate a significant financial return from the rising stock price (which an employee then benefits from when the RSUs vest at a higher price) even with “normalized employment”. Furthermore, in the event that an employee’s high-quality work significantly helps the company build better products, improve margins, and/or generate more revenue, then the employee’s work directly contributes to a rising stock price by “creating” returns, which aligns incentives.

From a financial perspective, it’s often logical to choose the company that has the greatest potential for the value of RSUs to increase over time. Coincidently, high-growth companies often also provide employees with lots of learning opportunities and opportunities to quickly enhance their skill sets.

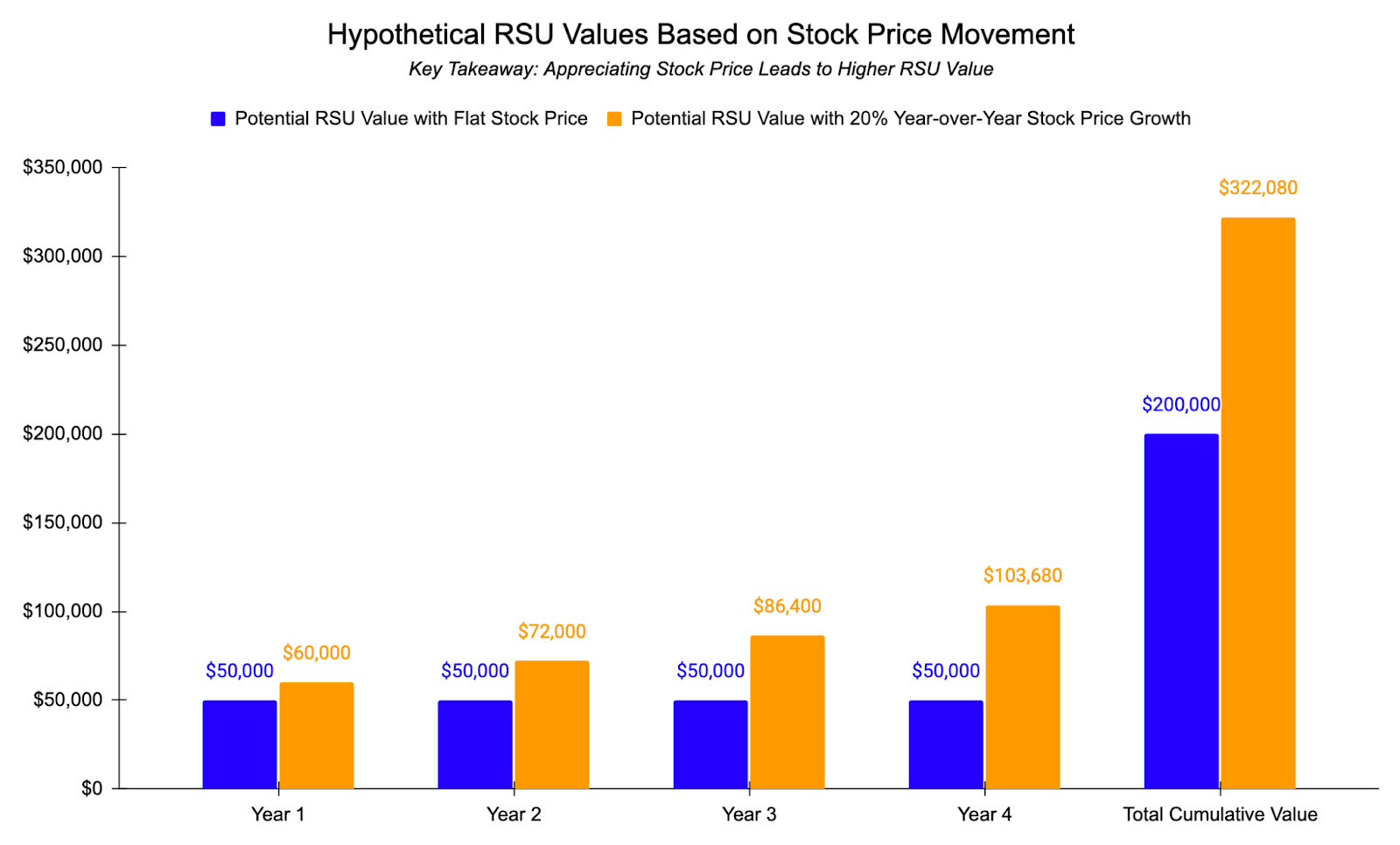

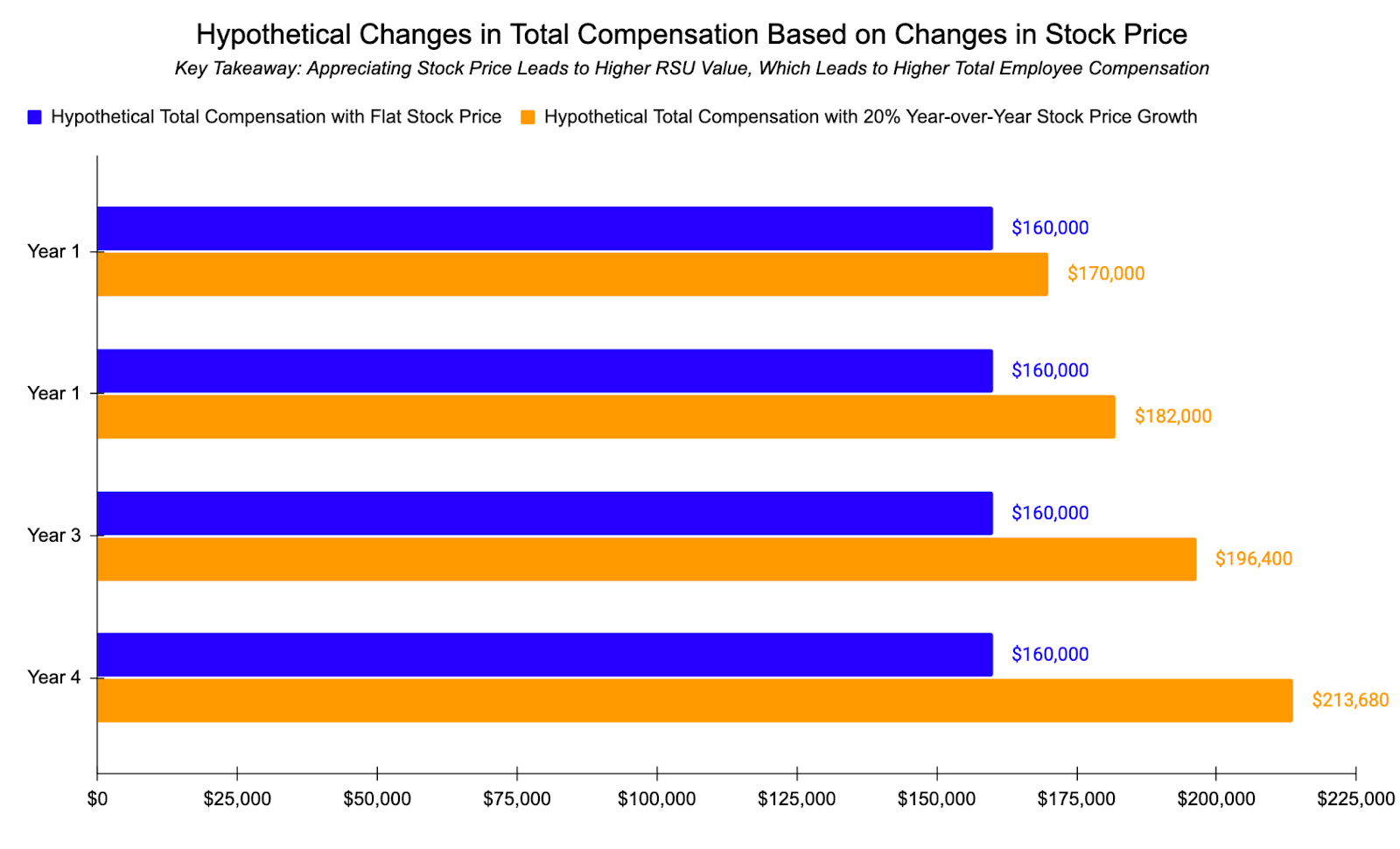

The following 2 charts below highlight 2 scenarios: Scenario 1 in blue highlights a flat stock price during the time of employment over 4 years, while Scenario 2 in orange highlights a stock price that increases 20% every year. Additionally, let us please assume in the scenario that a software engineer receives 2 identical offer letters from 2 different companies for a proposed $160K in total annual compensation with the following distribution: $100K annual base salary, $10K annual bonus, and $50K in annual RSUs. For the RSUs at the time of the offer letter, let’s assume that 10,000 shares are granted over 4 years at a stock price of $20 per share, which implies a $200K total RSU value at the time of the grant over 4 years if the stock price remains at $20 per share. Notably, while these are hypothetical in nature, there are a few assumptions:

Base salary, benefits, and bonus are assumed to remain the same over 4 years in calculating the estimates below. No additional stock grants (“stock refreshers”) are assumed for calculating the estimates below.

The employee is assumed to remain employed and in good standing in order to receive the RSU grants over 4 years.

While the estimates below assume an annual vesting schedule for RSUs, several companies offer quarterly or monthly RSU vesting schedules, which may alter the hypothetical calculations.

If a stock goes up 20% per year over 4 years, an employee receives a nearly 60% increase in the financial reward from the RSUs compared to the value of the RSUs at the time of the grant date.

When employees receive stock-based compensation and when the employer's stock price increases, this is a built-in increase in compensation to employees that is advantageous to employees. Conversely, when the employer's stock price decreases, total compensation for employees may decrease due to a declining RSU value.

5 Concluding Insights

Due to the financialization of total compensation for several software engineers and knowledge workers because of stock-based compensation, being a good stock-picker when choosing where to work adds value to one’s overall total compensation.

Understanding important software metrics is useful for investors, founders, and employees of software companies. Investors, stock-owning employees, and founders of software companies are aligned in that they are seeking high revenue growth that eventually commands dominant market share and significant enterprise value creation.

Often, revenue is a primary contributor to the valuations of software companies: How much is the revenue, how fast is the revenue growing, and how predictable & durable is this revenue?

Investors can use these software metrics to evaluate and invest in their view of high-quality software companies. Founders of software companies can use these metrics to benchmark their results, understand what’s important for investors (which is useful in increasing shareholder value and fundraising for additional capital), and find areas of improvement.

Switching jobs or changing companies may be akin to “buying the dip” of the new employer’s stock price, especially if equity grants across multiple offer letters are normalized in dollar terms, thereby providing a potential opportunity to receive more shares from a RSU grant via a lower stock price; hoping that the stock price recovers or grows in the future, then the RSU grant gains in value.

Stock-based compensation can be a key source in building financial wealth for employees. Choosing to work at high-growth companies with rising stock prices can potentially generate significant financial returns for share-owning employees via rising RSU values and rising prices of their existing investments & vested shares.

This letter is not an offer to sell securities of any investment fund or a solicitation of offers to buy any such securities. An investment in any strategy, including the strategy described herein, involves a high degree of risk. Past performance of these strategies is not necessarily indicative of future results. There is the possibility of loss and all investment involves risk including the loss of principal.

Any projections, forecasts and estimates contained in this document are necessarily speculative in nature and are based upon certain assumptions. In addition, matters they describe are subject to known (and unknown) risks, uncertainties and other unpredictable factors, many of which are beyond Drawing Capital’s control. No representations or warranties are made as to the accuracy of such forward-looking statements. It can be expected that some or all of such forward-looking assumptions will not materialize or will vary significantly from actual results. Drawing Capital has no obligation to update, modify or amend this letter or to otherwise notify a reader thereof in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate.

This letter may not be reproduced in whole or in part without the express consent of Drawing Capital Group, LLC (“Drawing Capital”). The information in this letter was prepared by Drawing Capital and is believed by the Drawing Capital to be reliable and has been obtained from sources believed to be reliable. Drawing Capital makes no representation as to the accuracy or completeness of such information. Opinions, estimates and projections in this letter constitute the current judgment of Drawing Capital and are subject to change without notice.